U.S. Sawmill Production Capacity Constant in 2024

Originally Published by: NAHB — March 19, 2025

SBCA appreciates your input; please email us if you have any comments or corrections to this article.

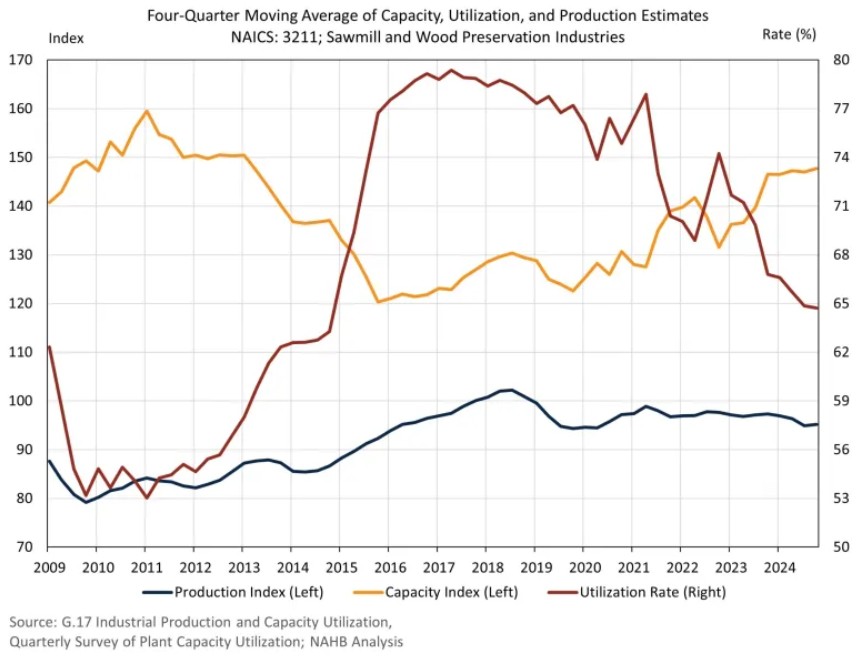

Sawmill and wood preservation firms reported lower capacity utilization rates coupled with level production and capacity throughout 2024. Despite no growth in production in 2024, utilization rates have trended downwards since 2017 as sawmills have expanded production capability. Even with more production capability, real output has not followed as output remains lower than 2018.

Capacity utilization rates are a ratio of actual production and potential production capabilities for firms. The utilization rate for sawmills and wood preservations firms was 64.7% in the fourth quarter on a four-quarter moving average basis. As utilization rates have shifted lower, the gap between full production capability and actual production has grown. Actual production is typically lower than full capability due to multiple factors ranging from insufficient materials and orders to lack of labor.

By combining the Federal Reserve’s production index and the Census Bureau’s utilization rate, we can compose a rough index estimate of what the current production capacity is for U.S. sawmills and wood preservation firms. Shown below is a quarterly estimate of the production capacity index. This capacity index measures the real output if all firms were operating at their full capacity.

Based on the data above, sawmill production capacity has increased from 2015 but remains lower than peak levels in 2011. Most of the recent capacity gains took place between 2023 and 2024, followed by little gain over the course of 2024. As evident above, there is ample room to increase production of domestic lumber, but current production levels remain much unchanged over the past several years.

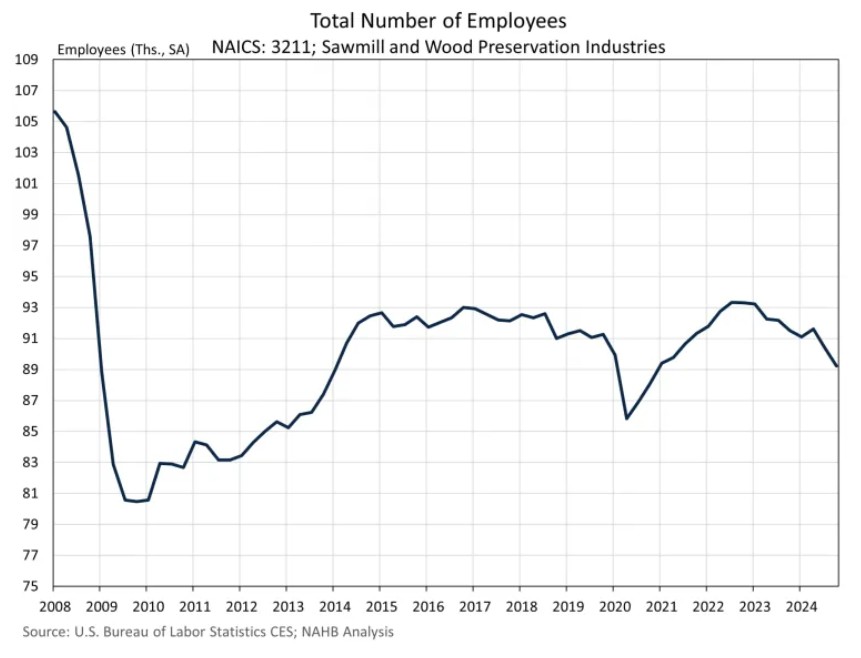

Employment is an important factor for ensuring firms reach their full capacity. For sawmill and wood preservation firms, the number of employees declined to its lowest level since 2021, reporting an average of just over 89,000 employees across the industry in the fourth quarter. Employment declines, likely due to a weak lumber market in 2024, help explain why utilization rates have fallen. With fewer workers, it is less likely that a firm can increase production to its full capability.

Imports

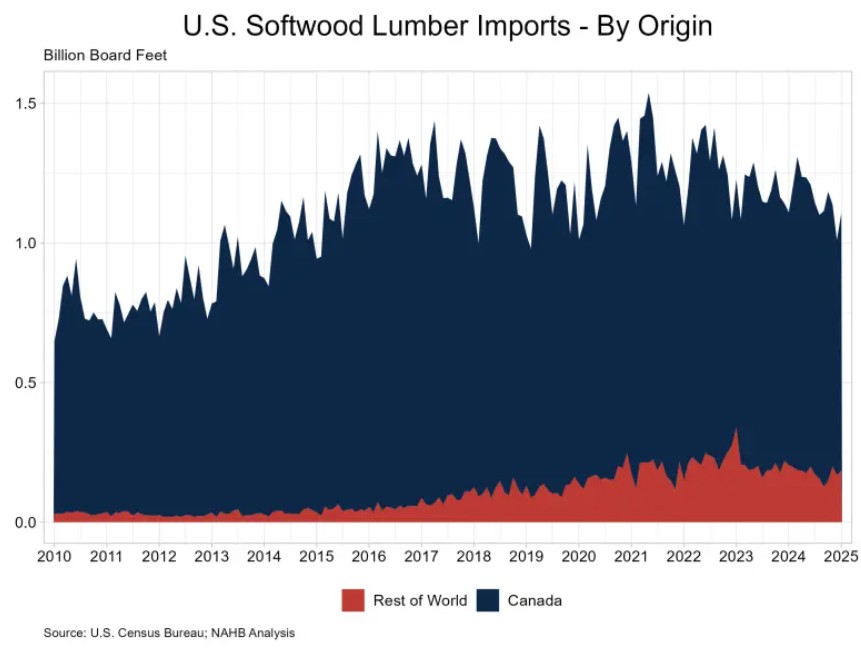

Since U.S. firms do not produce at their full potential, imports help to supplement domestic supply, especially in the softwood lumber market. According to Census international trade data, existing tariffs on Canadian softwood lumber have not reduced the need for imports to meet domestic consumption but have made the U.S. more reliant on non-North American lumber, resulting in unnecessarily complex supply chains. The current AD/CVD Canadian softwood lumber tariff rate stands at 14.5% and is expected to double under the administrative review process by the Department of Commerce. Potential tariffs on lumber, such as the ongoing 232 investigation and 25% on all Canadian goods, could push tariffs rates on Canadian softwood lumber above 50% later this year. Higher tariffs on softwood lumber mean higher costs for builders who use lumber as a key input to construction. Given the current housing unaffordability crisis, any additional costs will continue push homeownership and affordable housing further out of reach for households in the U.S.